Alfred Nobel, a Swedish chemist, engineer, and industrialist, is best known for his invention of the dynamite. However, the aftermath of this notorious creation led to a significant turning point in his life. Following the mistaken belief that he had passed away, Nobel came across a French newspaper article titled “The Merchant of Death is Dead,” which was referring to his brother’s demise. This incident, coupled with the negative media attention he received, deeply impacted Nobel, ultimately motivating him to revise his will.

In December 1896, just a year before his death, Nobel finalized his last will. Signed at the Swedish Norwegian club in Paris in November 1895, this document outlined his desire to utilize his fortune to establish prizes honoring individuals who have made the “Greatest benefit to mankind.” Thus, the Nobel Foundation was born, primarily tasked with managing the finances and administration of the prestigious Nobel Prize. The prize, created in various fields including Physics, Chemistry, Physiology, Literature, and Peace, serves to recognize those who have made significant contributions to the betterment of humanity. It is worth noting that in 1968, the Central Bank of Sweden, Sveriges Riksbank, funded the establishment of the Nobel Prize for Economic Sciences in the memory of Alfred Nobel. This addition expanded the Nobel Foundation’s scope and responsibilities. Why did the Nobel Foundation choose to award to someone who excelled in the field of Economics Sciences? But what exactly is Economic Sciences? Furthermore, why do Science and Mathematics hold such importance within the realm of Economics?

What is Economics?

Economics is a dynamic social science dedicated to the study of how societies, individuals, businesses, governments, and nations make decisions regarding the production, distribution, and consumption of goods and services. At its core, economics explores the complex web of choices and trade-offs involved in allocating scarce resources efficiently and effectively. Economists use theories, hypotheses, methods, and models to analyze economic behavior and phenomena. They develop economic models to explain and predict how individuals, companies, governments, and nations make decisions and policies, and how markets function. These models are backed by assumptions and simplified representations of reality, that allow economists to make better and reliable predictions and test their theories against real-world data and incidents.

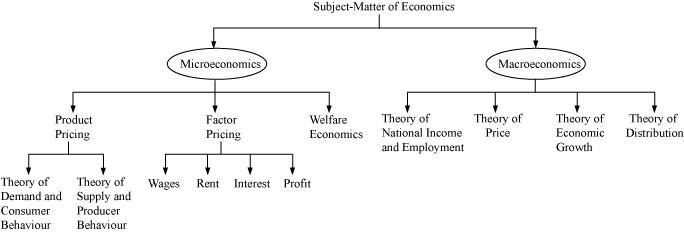

There are two main branches of economics such as microeconomics and macroeconomics.

Microeconomics –

Microeconomics studies how the decision-making processes of individual consumers and companies in resource management. Economists examine how these people and companies respond to price changes and the factors influencing their demand for goods and services. This branch of economics explores the complexities of valuation, financial decision-making, and trading behavior, making it clear to understand how individuals coordinate, cooperate, and engage in economic transactions. By analyzing the intersection of supply and demand, production costs, and labor allocation, microeconomics provides insights into the organizational structures of businesses and how individuals should manage uncertainty and risk when making decisions.

Macroeconomics –

Macroeconomics is the field of economics that examines the overall behavior and performance of an entire economy. It focuses on understanding recurring economic cycles, as well as much broader aspects of economic growth and development. This branch of economics examines various factors such as foreign trade, government fiscal and monetary policies, unemployment rates, inflation levels, interest rates, overall production output, and business cycles encompassing expansions, booms, recessions, and depressions. By utilizing aggregate indicators, economists employ macroeconomic models to inform the formulation of effective economic policies and strategies. These models assist in including the complex dynamics of an economy and guide decision-making processes at a broader level.

An economist is a person who examines the relationships between society’s resources, production, and output. And they give a better insight into the world and how this world we are living in functioning. Their opinions help to make better decisions on monetary policies, international and domestic trade agreements, tax policies, and risk management. They analyze and represent the economic indicators that can be used to detail the economic performances of entities such as countries, companies, and individuals as well. These economic indicators have a significant effect on stocks & bonds, employment, investment decisions, and international markets. When considering a country’s economic performance, some economic indicators are widely used. Such as Gross Domestic Product (GDP), Employment data, Industrial production, and Consumer Price Index (CPI). These economic indicators often predict the economic performance of a country and guide the governments to have better investment decisions that are crucial to the quality of life of the country.

Economic indicators are vital tools that provide insights into an economy’s health and guide decision-making. Over time, various economic systems have emerged, aiming to allocate resources efficiently and meet people’s needs. However, the journey of these systems has been marked by both progress and turmoil. They have had significant impacts on human affairs, influencing everything from family dynamics to devastating conflicts that have claimed countless lives such as revolutions and wars. These systems ensure that goods and services are produced, distributed, and consumed in an efficient and orderly manner. They help establish rules, incentives, and mechanisms for economic activities, promoting productivity, growth, and overall well-being. Economic systems also address the challenge of scarcity by allocating limited resources to fulfill needs and want. By imporving trade, investment, and specialization, economic systems contribute to wealth creation, job opportunities, and improved standards of living. These are five economic systems that illustrate the practices of resource management and allocation.

- Primitivism – a movement in art and thinking that appreciates and values the simplicity and close relationship with nature that existed in ancient cultures and early societies.

- Feudalism – a system during medieval times in Europe where powerful lords owned large lands and granted smaller portions to knights, who in turn provided military service and loyalty, while the rest of the population, called serfs, worked the land in exchange for protection and a place to live.

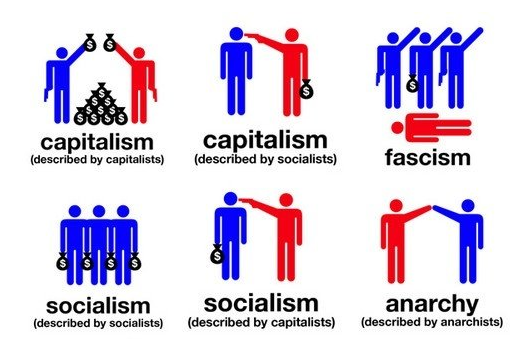

- Capitalism – a system where individuals and businesses own and control resources and industries, to make profits. In this system, competition and private ownership drive the economy, and people have the freedom to buy, sell, and invest based on their own choices and interests.

- Socialism – an economic system where the government plays a bigger role in controlling and distributing resources. In this system, the aim is to create a more equal society by ensuring that everyone has access to necessities like healthcare, education, and housing, and by reducing economic inequalities between different groups of people.

- Communism – a political and economic system where the government owns all resources and controls the means of production, aiming to create a society where wealth and power are shared equally among all members. In theory, it strives for a classless society where everyone’s needs are met, but in practice, it has often led to authoritarian governments and limited personal freedoms.

None of these systems are perfect, they all have their pros and cons in terms of promoting growth and fairness. But these are the economic systems that build the world around us throughout history. Understanding economic systems helps us make informed decisions about jobs, investments, and government policies, and can contribute to creating a more prosperous and equitable society for everyone.

These things seem to have no connection or interchange with science. But the truth is economics without science is gambling. The language of economics is mathematics. Science and mathematics play a crucial role in economics by providing a foundation of theoretical evidence, analytical tools, and methodologies for understanding and explaining economic phenomena.

Science helps economists identify causal relationships between variables and events. By applying scientific methods, economists can analyze data, conduct experiments, and establish cause-and-effect relationships to explain economic behavior and outcomes. This enables policymakers and researchers to make informed decisions, formulate effective economic policies and better investment strategies.

Science provides statistical and econometric techniques to analyze large sets of data. Through data analysis, then economists can identify patterns, trends, and correlations, enabling them to develop models that describe and predict economic behavior. These models serve as valuable tools for making forecasts, evaluating policy options, and understanding complex economic systems. With the rapid development of artificial intelligence and machine learning tools, this has been easier than ever.

Science contributes to the evaluation of economic policies by providing strong and effective methodologies for assessing their impact. Through randomized control trials, quasi-experiments, and other scientific techniques, economists can measure the effectiveness of policies, identify unintended consequences, and determine whether they achieve their intended objectives. This scientific approach helps policymakers make evidence-based decisions and refine policies for better outcomes.

Science helps economists analyze markets and understand how they function. Economic theories, based on scientific principles, provide insights into market efficiency, competition, and the behavior of economic agents. By studying human decision-making processes, economists can develop models of rational behavior and study how individuals, firms, and governments respond to incentives, leading to a better understanding of market outcomes. Therefore, there is broader involvement of science happening around the economic sciences field. Not only statistics, mathematics, and the scientific method, but there is also a significant amount of involvement in behavioral sciences such as psychology and human behavior. Especially to have a better understanding of the financial markets economists should have a good understanding of human behavior and the human decision-making process. With the wide usage of social media, a single photo or a tweet is enough to make a random company a billion dollars or a billion-dollar conglomerate lose a few billion dollars and get bankrupt.

Science contributes to the understanding of economic growth and development by examining factors that influence productivity, innovation, and technological progress. Through scientific research, economists can identify policies and interventions that foster economic growth, alleviate poverty, and promote sustainable development. This knowledge helps countries make informed decisions to enhance their economic performance and improve living standards.

And Science provides tools for analyzing risk and uncertainty in economic decision-making. Economic research utilizes probability theory, statistical analysis, and other scientific methods to assess and manage risks in various economic activities, such as investment, finance, and insurance. This helps individuals, businesses, and policymakers make informed choices under conditions of uncertainty. As an example, having a solid understanding of nature, which includes studying various scientific aspects, can greatly benefit stock traders and investors. For instance, by analyzing rain and cyclonic patterns, one can make informed investment decisions in the energy sector, potentially leading to substantial financial gains. Similarly, knowledge about diseases, virus outbreaks, their potential cures, and the pharmaceutical industry can aid in identifying investment opportunities and potentially reaping significant returns. Investing is all about taking correct decisions at the most appropriate times. Therefore, having a grasp of science can play a crucial role in making wise investment choices and potentially achieving financial success.

Overall, science and economics are closely intertwined. The scientific approach provides economists with the tools and methods to study, understand, and improve economic systems. By embracing scientific principles, economics becomes a more evidence-based and rigorous discipline, enabling policymakers and researchers to make more accurate predictions, evaluate policies effectively, and promote economic well-being. Having a dedicated prize, such as the Nobel Prize in Economic Sciences, holds great significance. It recognizes the importance of economics as a distinct field of study and highlights its impact on society. By awarding individuals who have made significant contributions to the understanding of economic systems, this prestigious prize encourages further advancements in economic theory and policy. It not only honors the achievements of outstanding economists but also inspires others to pursue innovative research and ultimately contribute to the betterment of global economies and human well-being. And all these outstanding achievements cannot be possible without the vast range of scientific and mathematical theories, methodologies, and explanations. Therefore, the role of science that plays in economics is unquestionable and undoubtful.

Image courtesies:

Cover image – http://bitly.ws/LxEf

Image 1 – http://bitly.ws/LxEs

Image 2 – http://bitly.ws/LxEz

Image 3 – http://bitly.ws/LxEP

Image 4 – http://bitly.ws/LxEX

Image 5 – http://bitly.ws/LxF2

Image 6 – http://bitly.ws/LxFj

Image 7 – http://bitly.ws/LxFu

Image 8 – http://bitly.ws/LxFG